Your credit score and report help lenders get a general sense of the health of your business and, ultimately, your ability to repay a loan. If the information in your credit report indicates that you’re a reliable borrower, lenders will typically be more likely to work with you and give you a more attractive interest rate.

There are a few important elements to your credit report. Here’s how they play a role in your report, and why they’re so vital to improving your credit.

What is credit reporting?

Your credit reports are generally comprised of your:

- Current debt

- Bill payment history

- Loans

- Other relevant financial details

They may also show other personal information, like if you’ve ever experienced things like filing for bankruptcy or being sued or arrested.

As a small business owner, this information is essential because it gives vendors, partners, and other business entities an idea of how likely you are to pay back a loan. More specifically, credit scoring tells them how likely it is that you’ll be more than 90 days late making a loan payment. The better your score, the more probable it is that you will make payments on time, and the more secure financial institutions will feel in lending you money. A lower score typically makes it harder to secure a loan and may mean higher interest rates or less favorable terms.

Where do credit reports come from?

Credit reports come from bureaus or agencies. These entities collect data about your business, your payment history, and your general background. Then, they sell this information to creditors, employers, insurers, and other businesses that might need to evaluate your application for credit, insurance, employment, or renting.

There are three major credit bureaus in the United States:

- Equifax®

- TransUnion®

- Experian®

Lenders typically pull data about their loan applicants from one or more of these agencies. SmartBiz® works specifically with Experian.

Who provides business credit reports?

Similar to you as an individual, your business has its own credit score and report. These reports are provided by three main agencies:

- Dun & Bradstreet®

- Equifax

- Experian

Many of the things you do to improve your personal credit score may apply to your business credit score, too. For example, you should consider paying back your bills on time, every month to increase the chances of obtaining a positive credit score.

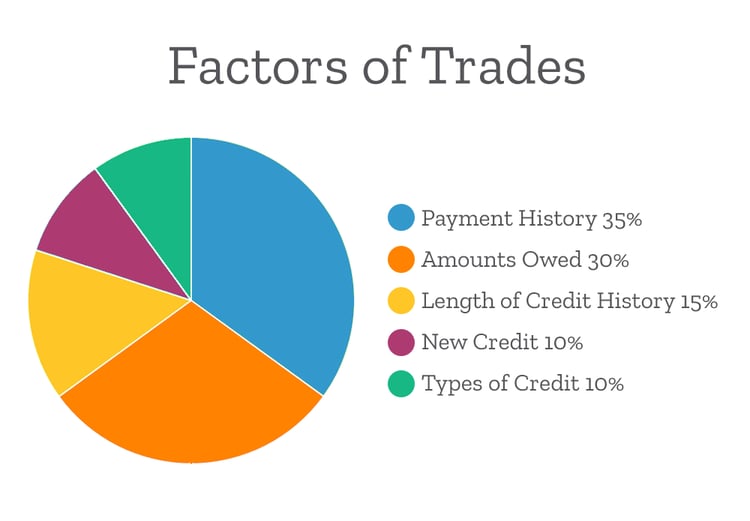

What is a FICO score?

FICO stands for Fair Isaac Corporation. A FICO score is a type of credit score based on five main factors:

- Payment history

- Current debts

- Length of credit history

- New credit accounts

- Types of credits used

Each factor is weighed differently. Here’s how it generally breaks down:

All of the factors play a role. For instance, longer credit history can increase your FICO score, but it’s only worth 15% of the calculation. Even people with a very short credit history may have a high FICO score, depending on what the other factors look like for them.

Assessing the FICO score

In order to determine your FICO score, you need:

- One credit account that’s been opened for at least six months

- One credit account that’s reported within the last six months

Want to dive into this deeper? Learn more about how to determine your FICO credit score. Note that banks who partner with SmartBiz typically evaluate an applicant’s reports based on three main segments:

- Public records

- Past and current trade lines

- Credit inquiries

What role do public records play in your credit score?

When a public record is filed, it can be found with a local, county, or state federal court. But what is it, exactly? It almost always reflects something like bankruptcy, judgment, foreclosure, or a tax lien. Thus, a public record is often something that may lower your credit score.

What are trade lines?

A trade line refers to any record of activity for any credit that a lender has extended to a borrower. It also includes information like your payment history, including late or missed payments, how recently they occurred, how frequent they are, and how much you were supposed to pay.

The major types of trade lines are typically:

- Revolving lines of credit: This is credit that has a limit, and you can borrow up to that limit without needing to reapply for more. A credit card is an example.

- Installment lines of credit: This is a single loan disbursement that requires periodic payments. An example is a student loan.

Regardless of the type of trade line you’re utilizing, you’ll generally want to keep these things in mind:

- Credit utilization: This percentage reflects how much credit you’re using out of what is available to you. High credit utilization may hurt your credit score, so only borrow what you really need.

- The number of new accounts you’re opening: If you’re opening several accounts—and especially if you’re maxing them out—this tells lenders that you’re probably not in a place to take on even more debt.

What are credit inquiries?

When a lender requests your credit report, it’s called a credit inquiry. There are two types:

- Soft inquiries (AKA soft pulls): Soft inquiries are usually pulled earlier on in the application process so that you can determine what type of funding you qualify for. These typically do not affect your credit score and don’t appear on your report. The tradeoff is that they provide the lender with less information. SmartBiz conducts a soft credit pull that will not affect your credit score.* However, in processing your loan application, the lenders in our network will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull.

- Hard inquiries (AKA hard pulls): These appear on your credit report for two years and affect your score for 12 months. A higher number of hard inquiries typically tells a lender that you may be a riskier borrower.

Learn more about hard vs soft inquiries.

What is a liquid credit score?

The FICO Liquid Credit Score is a combination of your personal and business credit scores, and it ranges from 0 to 300. This score further gives lenders an idea of a business’s overall financial health and makes it possible for them to process applications faster. FICO calls this their Small Business Scoring Service (SBSS). They use this to help rank business applicants by their likelihood to make their payments on time.

SmartBiz bank partners use this score during the pre-screening process. Note that if you’re applying for an SBA 7(a) loan, it’s required. Learn more about how to improve your SBSS score.

What is E-Tran Scoring?

E-Tran is the SBA’s scoring system. Lenders will use it to determine if the SBA will allow them to lend money under their delegated authority. It’s a bit mysterious because the SBA hasn’t released exactly what determines it. We do know that scores range from 0 to 300, and you need at least 140 to pass. If you pass, the lender can move forward to fund the loan. If you don’t pass, the lender may likely still move forward but must follow the SBA’s requirements for loans over $350,000, which includes full collateralization of the loan. This means that you need to put a valuable asset on the line in order to secure the loan.

In Conclusion

The various ways of gathering information about credit history help lenders evaluate the risk associated with an individual’s unique loan application. When you work with SmartBiz, you’ll have a dedicated representative who can answer your credit questions.

To stay on top of your credit score, you should consider checking your credit report throughout the year. As an individual, you can typically get one free copy of your credit from Equifax, Experian, and TransUnion every 12 months. Businesses must generally pay a fee to get their credit report.

In taking proactive steps to improve your credit score, you may have better access to loans that have low rates, long terms, and lower monthly payments.