The Small Business Administration (SBA), a government agency created in 1953, was founded to "aid, counsel, assist and protect, insofar as is possible, the interests of small business concerns.”

Just one year later, the SBA already was making direct business loans, guaranteeing bank loans to small businesses, helping business owners secure government procurement contracts and offering training, management assistance and technical help.

Here are funding options offered.

What are the available SBA loan programs?

The most prominent assistance program that the SBA offers is a guarantee on loans made through banks, credit unions, and other lenders they partner with. By securing a portion of the loan in the case of the borrower defaulting, the lenders are presented with less risk so they are more likely to offer an affordable loan. Since 2009, the SBA has backed over $150 billion through its various programs. Here are the loan programs currently offered by the SBA.

SBA 7(a) loans

By far the agency’s most popular loan program, SBA 7(a) loans have low rates and long terms, leading to small monthly payments. Proceeds from an SBA loan can be used in a wide variety of ways. Working capital, high-interest existing debt refinance, and Commercial Real Estate purchases and refinance. For detailed information about these loans in high demand, visit the SmartBiz Loans website: SBA loans: The gold standard in small business lending.

CDC/504 Loans

The 504 Loan Program was created to give small businesses low cost funds for expansion or modernization. Typically, up to 50% of project costs are funded by a lender backed by the SBA. CDCs (Community Development Corporations) typically fund up to 40% of the project cost. The final 10% is a cash down payment expected to come from the small business owner.

CAPLines of Credit

The CAPLines Program allows small businesses to acquire lines of credit, fixed or revolving, to help meet short term working capital needs. For example, it can help businesses cover expenses during slow times. CAPLines of credit are offered by SBA approved lenders and guaranteed in part by the SBA.

Disaster Loan Program

The SBA offers low-cost loans to businesses of all sizes, private non-profit organizations, homeowners and renters in disaster affected areas. Funds from an SBA disaster loans can be used to repair or replace an approved list of items damaged or destroyed in a declared disaster. Visit the SBA website to review their disaster loan program facts sheet.

Benefits of an SBA 7(a) loan

The advantages of SBA loans include:

1. Low Interest Rates

Interest rates for SBA loans are essentially as low as they get. Your interest rate will depend on your own creditworthiness and the qualifications you demonstrate. Unlike other types of term loans, you won’t see interest rates climbing into the double digits.

2. Low Monthly Payments

Because of the long terms of an SBA 7(a) loan, monthly payments are very small. This helps you manage cash flow and avoid struggling to meet your obligations.

3. Capital Availability

An advantage of SBA loans is the access to capital allowed. You can borrow up to $5 million, which means that borrowing the capital you need is possible.

4. Repayment Terms

One key advantage to SBA loans is their terms: longest repayment terms, (10 years for a working capital loan, 25 years for a commercial real estate loan) and a payment schedule that shouldn’t put financial strain on your business.

5. Flexibility of Use

With an SBA 7(a) loan, you can use the funds for almost anything. The terms of use for SBA 7(a) funds are pretty broad—you can refinance existing debt, buy land, purchase inventory, make upgrades.

What is an SBA 7(a) loan and how to get one

SmartBiz Loans has helped thousands of business owners acquire a low-cost SBA loan. In fact, about 90% of SBA loan applications referred to our bank partners are approved. Here are details about how to successfully go through the application process.

- Time in Business: 2+ Years

- Business owners must be U.S. citizens or legal permanent residents

- Credit Score: Business owners must have personal credit scores above 650 (675 for Commercial Real Estate SBA loans)

- Cash Flow: Sufficient business and personal cash flow to service all debt payments demonstrated by tax returns and interim financial data

- Public Records: No bankruptcies or foreclosures in the past 3 years; no outstanding collections; no open tax liens

- SBA Specific Requirements: no delinquencies and/or default on government loans

Eligibility requirements for a SmartBiz SBA 7(a) commercial real estate loan are:

- The real estate must be majority owner-occupied. This means at least 51% of the square footage of the property you’re buying or refinancing must be occupied by and used by your business.

- Time in Business: 2+ Years

- Business owners must be U.S. citizens or legal permanent residents

- Credit Score: Business owners must have personal credit scores above 675

- Cash Flow: Sufficient business and personal cash flow to service all debt payments demonstrated by tax returns and interim financial data

- Public Records: No bankruptcies or foreclosures in the past 3 years; no outstanding collections; no open tax liens

- SBA Specific Requirements: no delinquencies and/or default on government loans

Prepare required paperwork

Your next step is to start preparing. No matter which lender you’re working with, having all the necessary documentation is crucial to obtaining your funds as quickly and efficiently as possible. At SmartBiz, you set the pace when it comes to completing the SBA loan application. The more readily available your documentation is, the faster we can help you get to a “Yes” from one of our lending partners.

As you’re progressing through the application, you’ll need to demonstrate that you’re able to make regular payments. Some of the most common documents that our partner banks request include:

- Personal & Business Tax Returns

- Personal Financial Statements, required from each individual owning 20% or more of the company

- Profit and Loss Statement

- Balance Sheet

- Collateral

Visit the links above from the SmartBiz Small Business Blog for explanations and how to prepare each requirement.

Connect with an SBA Loan Lender

Once you’re prepared to answer questions and your paperwork is in order, you’re almost ready to apply for funding. Before you do, you’ll need to find a provider who can package and service the loan. That’s where SmartBiz comes in. We’ll help you increase your chances of getting a “Yes” from one of our lending partners by matching you with the bank partner most likely to fund your particular business profile. Don’t waste time going from bank-to-bank. Start an SBA 7(a) loan application.

Additional SBA Resources: Office of Entrepreneurial Development

In addition to funding, this agency is fulfilling their mission to help small businesses start, grow, and compete by providing quality training, counseling, and access to resources. The programs and services offered include:

Small Business Development Centers (SBDCs)

The SBDC program offers management and business counseling services. The SBDC are the SBA’s largest non-financing program and is a collaboration of SBA funding along with state and private resources. Currently, more than 950 service centers handle counseling and training needs of roughly 650,000 clients annually.

Manufacturing, procurement, technology transfer, disaster recovery, technology, market research and international trade are emphasized. To learn more about the SBDC program or to locate an SBDC near you, visit the SBA's website.

Office of Women's Business Ownership

The Office of Women’s Business Ownership’s mission is to enable and empower women entrepreneurs. Economically or socially disadvantaged women are offered training and counseling in many languages to help them start and grow their own businesses.

Office of Entrepreneurship Education

Here’s the mission statement of this office:

“The Office of Entrepreneurship Education's mission is to provide entrepreneurial information and education, resources and tools to help small businesses succeed. The office is an integral component of Entrepreneurial Development's network of training and counseling services.”

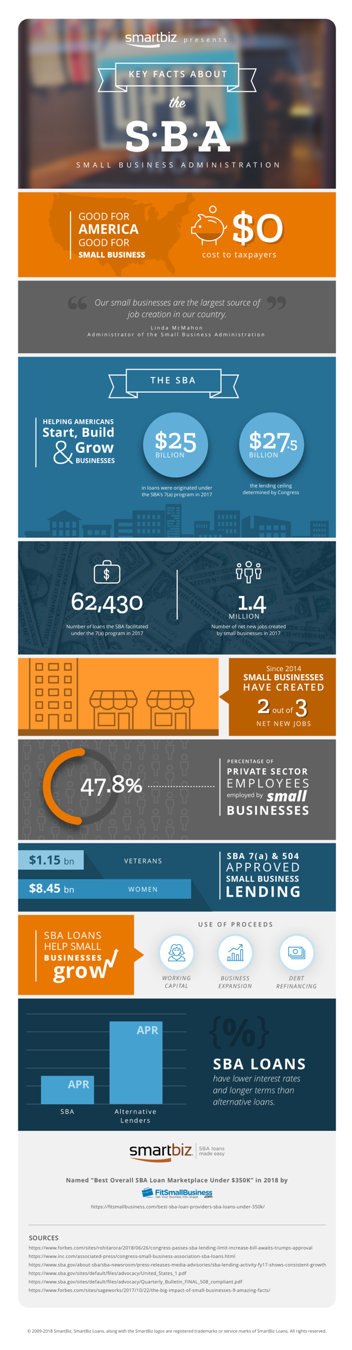

SBA Infographic

It’s clear that the SBA has the small business owner’s interests front and center. For more insight into the SBA, check out our “Key Facts the SBA” infographic below.